The coronavirus has taken the world, and the U.S. economy, by storm. After the longest bull market in history, the stock market is now deep in bear market territory.1 Businesses, sports, leagues, and schools have shut down. This is an unprecedented time in American history, but it should continue for at least a bit longer. On March 29, President Trump extended the nation’s social distancing guidelines through the end of April.2

We can’t predict when life will get back to normal or when the economy may recover. However, you can take action to minimize your exposure to future risk and to take back control of your financial future. Below are a few steps to consider during this volatile time: Review your strategy. When’s the last time you reviewed your retirement strategy? Many people become more risk-averse as they become older, even without the threat of coronavirus. If you haven’t adjusted your strategy in years, now may be the time to do so. It may be time to take a more conservative approach. A financial professional can help you determine if your current strategy is still right for your needs and goals. We can offer virtual consultations to help you review your strategy from the comfort and safety of your home. Protect your retirement income. Are you planning on taking retirement withdrawals from your savings? If so, now could be the time to protect that income so it continues for life, no matter what threats may arise in the future. For instance, you can use annuities to create guaranteed* lifetime streams of income. The income continues as long as you live, no matter how the coronavirus or any other risk affects the economy. Consider risk protection tools. There some types of annuities that allow you to earn interest based on a stock market index’s performance. If the index performs well, you may earn more interest. If it performs poorly, you don’t lose money. Again, a financial professional can help you determine if these tools are right for you. Ready to protect your nest egg from market volatility? Let’s talk about it. Contact us today at Financial Solutions Group. We can help you analyze your strategy. Let’s connect soon and start the conversation. 1https://finance.yahoo.com/news/stock-market-news-live-march-12-013620137.html 2https://www.cnn.com/2020/03/29/politics/trump-coronavirus-press-conference/index.html Licensed Insurance Professional. This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation. By providing your information, you give consent to be contacted about the possible sale of an insurance or annuity product. This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. This information has been provided by a Licensed Insurance Professional and is not sponsored or endorsed by the Social Security Administration or any government agency. Investing involves risk, including the loss of principal. No Investment strategy can guarantee a profit or protect against loss in a period of declining values. Any references to protection benefits or lifetime income generally refer to fixed insurance products, never securities or investment products. Insurance and annuity products are backed by the financial strength and claims-paying ability of the issuing insurance company. Any transaction that involves a recommendation to liquidate funds held on securities product, including those within an IRA, 401(K) or other retirement plan, for the purchase of an annuity, can be conducted only by individuals currently affiliated with a properly registered investment advisor. If your financial professional does not hold the appropriate registration, please consult with your own broker/dealer representative or registered advisor for guidance on your securities holdings. Guaranteed lifetime income available through annuitization or the purchase of an optional lifetime income rider, a benefit for which an annual premium is charged. Guarantees provided by annuities are subject to the financial strength of the issuing insurance company; not guaranteed by any bank or the FDIC. 19952 - 2020/3/30  On March 27, President Trump signed the Coronavirus Aid, Relief, and Economic Security Act, which provides economic support to Americans who have been impacted by the coronavirus pandemic. You’re probably familiar with the highlights of the bill:

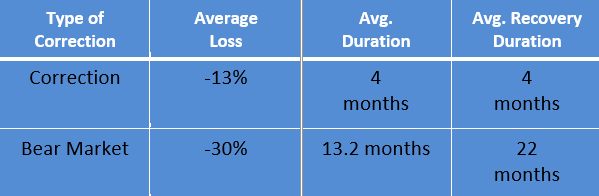

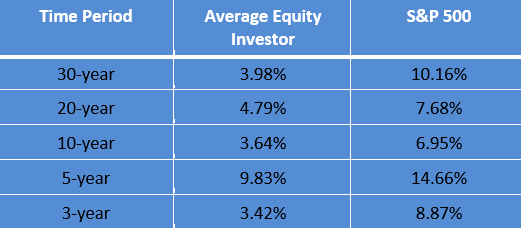

Those components are important and will certainly help many people get through this unprecedented period. However, there are some other provisions that could be important for you, especially if you’re approaching retirement or are already retired. Extended Tax Filing and IRA Deadline The IRS pushed back the tax filing deadline to July 15 from the traditional April 15.2 That gives you more time to prepare your return, collect documents, and possibly implement a strategy to minimize your tax bill. That also gives you more time to contribute to your IRA. You can make an IRA contribution up to July 15 and count it as a deduction on your 2019 return, assuming of course that you meet income requirements.3 401(k) and IRA Distribution Options It’s possible that you may need additional funds to get you through this period, especially if you or your spouse have been furloughed or have lost income. The CARES Act allows you to tap into your qualified retirement accounts through special distributions. You can take a withdrawal from your 401(k) and IRA without paying the 10% early distribution penalty, even if you are under age 59 ½. The distributions are taxable, but the taxes are spread over a three-year period. However, you can also repay the distribution over that three-year period and avoid paying taxes on the distribution.3 While a 401(k) or IRA distribution may be helpful, it could also have long-term consequences. When you take a distribution from your account, those funds are no longer invested. That means those funds can’t compound and grow. It’s possible that you may not fully participate in a market recovery if you decide to take a distribution, which could hurt your long-term growth. Waiver of RMDs Are you required to take an RMD in 2020? Not anymore. The CARES Act waives all RMDs in 2020, so there is no penalty for not taking a minimum distribution from a 401(k) or IRA. 4 This could be very helpful for your account balance. Your RMD would have been based on your December 31, 2019. Depending on how you are allocated, your account value may have been significantly higher on that date than it is today. That means that had the RMD not been waived, you would have potentially been required to take a substantial withdrawal from an account that had fallen in value.4 This may be a confusing and unprecedented time, but you have options available. We are here to help you explore those options and implement the right strategy for your retirement needs and goals. Contact us today at Financial Solutions Group. Let’s connect and start the conversation. 1https://www.thebalance.com/2020-stimulus-coronavirus-relief-law-cares-act-4801184 2https://www.irs.gov/coronavirus 3https://www.marketwatch.com/story/this-is-how-the-2-trillion-coronavirus-stimulus-affects-retirees-and-those-who-one-day-hope-to-retire-2020-03-31 4https://www.aarp.org/money/investing/info-2020/cares-act-retiree-tax-benefit.html Licensed Insurance Professional. This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation. By providing your information, you give consent to be contacted about the possible sale of an insurance or annuity product. This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. This information has been provided by a Licensed Insurance Professional and is not sponsored or endorsed by the Social Security Administration or any government agency. 19977 - 2020/4/7  The 2020 election cycle is in full swing. It’s primary season, which means the general election is right around the corner. Before you know it, the two major parties will have their conventions and we’ll be heading to the ballot box. Of course, you may already have election fatigue. From the local level all the way up to national races, candidates are already flooding television with political ads. As is the case in most presidential elections, candidates are also talking about the economy. They may make claims about what will happen in the economy if they’re elected or that the markets might decline if their opponent is elected. That kind of rhetoric is common during elections, but is it accurate? Will the outcome of the election impact your portfolio? Should you worry about the election? Or perhaps even change your allocation to protect yourself. Below are a few tips to keep in mind through the rest of the election year: Keep history in perspective. Often when there is one issue or story dominating the news, like the presidential election, it’s easy to focus solely on that story. It’s in the news and on social media so much that it feels like it’s the most important issue in the world. However, the truth is that this country and the stock market have been through many presidential elections. In fact, in most of those years, the markets performed positively. In fact, since 1928, there have been 23 presidential elections. In 19 of those years, the S&P 500 had a positive return.1 In fact, in the four instances when the markets did have negative returns, there were also economic events happening that may have driven the performance. In 1932, the country was in the midst of the Great Depression. In 1940, the country was entering World War II. The markets declined in 2000, which was the year George W. Bush ran against Al Gore. However, the bursting tech bubble in Silicon Valley may have had more influence on the markets than the election. Finally, in 2008, the S&P 500 also declined, but that was the year of the financial crisis. The takeaway is that market declines can happen in any year. The fact that it’s an election year may cause news stories and rhetoric, but the market is likely driven by investor concerns and economic conditions. Focus on the long-term. Your investment strategy was likely designed for the long-term. Perhaps you’re saving for retirement or some other goal that is years or possibly even decades in the future. Over that period, you’ll likely see times of market volatility. Whether it’s an election year or not, it’s always helpful to focus on the long-term during challenging periods. Market downturns happen, but they are always temporary. There are two common types of downturns: corrections and bear markets. Corrections are losses of 10% or more. Bear markets are losses of 20% or more. As you can see in the chart below, the average correction loses around 13% and the average bear market sees a loss of around 30%.2 However, the duration of each is also important. A correction, on average, lasts around four months. After that period, there is an average four-month recovery period to recoup the losses. Bear markets last longer. They have an average duration of 13 months with a 22-month recovery period.2  Market downturns are never pleasant, but they are temporary. Keep an eye on the long-term and stick to your strategy. Don’t make gut decisions. It can be easy to make a gut, impulse decision when you hear and see stressful news on a regular basis. It might be tempting to sell your investments and move to asset classes that have less risk and volatility. However, a move to perceived safety could do more harm than good. The chart below shows how the average equity investor has fared compared the S&P 500 over different periods of time. As you can see, the index always wins, sometimes by a wide margin. 3  Why does this happen? Primarily because the index stays invested at all times, while the average investor is constantly moving in and out of the market based on gut decisions or attempts to avoid loss. While investors may miss some declines with this strategy, they also miss out on gains. Staying invested usually leads to better long-term performance.

Ready to protect your portfolio this election year? Let’s talk about it. Contact us Financial Solutions Group. We can help you analyze your needs and develop a strategy. Let’s connect soon and start the conversation. 1https://www.thebalance.com/presidential-elections-and-stock-market-returns-2388526 2https://www.cnbc.com/2018/12/24/whats-a-bear-market-and-how-long-do-they-usually-last-.html] 3https://www.marketwatch.com/story/americans-are-still-terrible-at-investing-annual-study-once-again-shows-2017-10-19 Licensed Insurance Professional. This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation. By providing your information, you give consent to be contacted about the possible sale of an insurance or annuity product. This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. This information has been provided by a Licensed Insurance Professional and is not sponsored or endorsed by the Social Security Administration or any government agency.  It’s been a volatile few weeks in the financial markets. Up until late January, we were still enjoying the longest bull market in history. In three short weeks, the bull market has ended, and we’ve entered bear market territory. Between Friday, February 21 and Monday, March 16, the Dow Jones Industrial Average has dropped by 30.37%.1

The rapid decline has left many investors with two questions:

There’s no easy answer to the first question. If history is any guide, eventually the decline will stop, and the markets will recover. The average bear market lasts 13 months, followed by a 22-month recovery.2 However, it’s impossible to predict when that recovery might begin. The second question is even more difficult to answer. There are certainly protection options available, but not all options are right for all investors. Your strategy should be based on your unique needs, goals, and tolerance for risk. Below are a few options you have available: Shifting to a more conservative allocation. Changing your allocation to a more conservative strategy is always an option. Many people become more risk averse as they approach retirement. If you haven’t reviewed your allocation in years, this may be the right time to do so. Of course, a more conservative allocation could limit your participation in a recovery when it happens. Work with a financial professional to find an allocation that limits your exposure to further losses, but still gives you an opportunity to participate future upside. Staying the course. Another option is to stay the course and stay invested in your current allocation. Again, that may expose you to further losses, but it could also put you in a position to take advantage of a recovery when it does happen. Again, it’s impossible to predict when a recovery could happen, but history can provide some insight. The last bear market started in October 2007 and lasted until March 2009, spanning much of the financial crisis. The S&P 500 dropped 56.8%. However, the subsequent bull market (which just ended) lasted more than 10 years and saw the S&P 500 increase by more than 400%.3 The 2000 bear market was triggered by the tech bubble. It lasted nearly 30 months and saw a total decline of more than 49%. It was followed by a 60-month bull market with a return of more than 100%. The 1990 bear market lasted only three months and had a decline of 20% and it was followed by a 113-month bull market with a cumulative return of 417%.3 Bear markets are often followed by bull markets. The question is whether you can stick it out through further losses. Again, your financial professional can talk through your options with you and help you decide which path is right. Use risk-protection vehicles. Another option is to take advantage of market risk-protection vehicles like fixed annuities. There is a wide range of different types of annuities that can limit your exposure to market risk and protect your future. For example, some guarantee your principal against loss, but also offer upside growth potential. Others guarantee your future retirement income, no matter how the market performs in the future. A financial professional can help you determine if an annuity or other risk-protection tool is right for you. Ready to protect your nest egg from the coronavirus? Let’s talk about it. Contact us today at Financial Solutions Group We can help you analyze your investments and implement a strategy. Let’s connect soon and start the conversation. Annuities contain limitations including withdrawal charges, fees and a market value adjustment which may affect contract values. Annuities are products of the insurance industry; guarantees are backed by the claims-paying ability of the issuing company. Guaranteed lifetime income available through annuitization or the purchase of an optional lifetime income rider, a benefit for which an annual premium is changed. 1https://www.google.com/search?safe=off&sa=X&tbm=fin&sxsrf=ALeKk02Fk2yPH2_A7nU0wQGE5IUIixHyGQ:1584394531365&q=INDEXDJX:+.DJI&stick=H4sIAAAAAAAAAONgecRozC3w8sc9YSmtSWtOXmNU4eIKzsgvd80rySypFBLjYoOyeKS4uDj0c_UNkgsry3kWsfJ5-rm4Rrh4RVgp6Ll4eQIAqJT5uUkAAAA&ved=2ahUKEwiBmOfJ-Z_oAhWUW80KHc2dA3MQ3N8BMAJ6BAgCEAM#scso=_SfFvXsWJMJe1tAbX6pm4BQ1:0 27https://www.cnbc.com/2018/12/24/whats-a-bear-market-and-how-long-do-they-usually-last-.html 3https://www.cnbc.com/2020/03/14/a-look-at-bear-and-bull-markets-through-history.html Licensed Insurance Professional. This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation. By providing your information, you give consent to be contacted about the possible sale of an insurance or annuity product. This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. This information has been provided by a Licensed Insurance Professional and is not sponsored or endorsed by the Social Security Administration or any government agency. 19926 - 2020/3/17 |

Archives

November 2020

Categories

All

|

RSS Feed

RSS Feed

Thomas B. Scarpaci Jr., partnerJoseph D. Sciarrino, CPA, partner |

Site Map |

This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation.

Securities and Advisory Services offered through CfreativeOne Securities, LLC Member FINRA/SIPC and an Investment Advisor. Financial Solutions Group, LLC and CreativeOne Securities, LLC are not affiliated.

This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

Check the background of an investment professional.

Securities and Advisory Services offered through CfreativeOne Securities, LLC Member FINRA/SIPC and an Investment Advisor. Financial Solutions Group, LLC and CreativeOne Securities, LLC are not affiliated.

This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

Check the background of an investment professional.