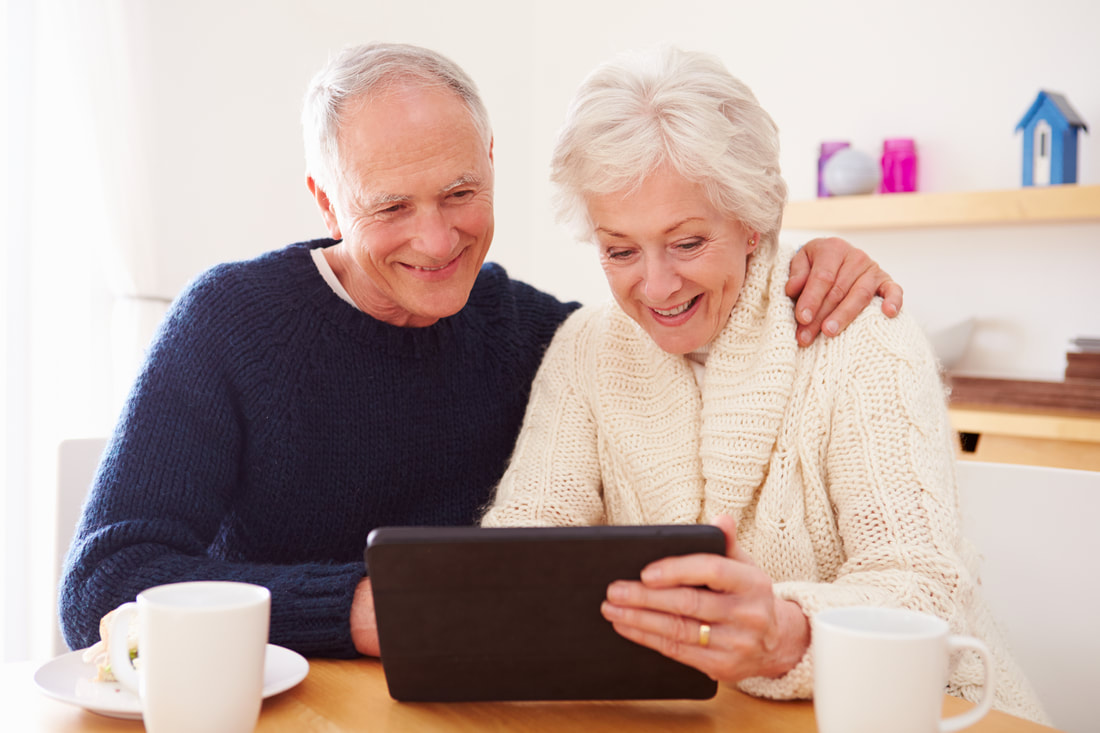

Think long-term care insurance could be right for you? That may be a smart decision. The U.S. Department of Health and Human Services estimates that today’s 65-year-olds have a 70 percent chance of needing long-term care at some point.1

Long-term care is ongoing assistance with basic, day-to-day living activities such as bathing, eating, mobility and more. It’s usually provided in an assisted living facility, but it can also be provided in the home, either by family members or by in-home health aides. Regardless of where the care is provided, it’s usually a costly service. Long-term care often costs thousands of dollars per month, and care is often needed for years. It’s easy to see how it can be a long-term drain on your savings.

0 Comments

The year is halfway over. Are you on track to hit your savings goals? If not, don’t worry. It’s easy to get off track with your savings, especially when it comes to a long-term goal like retirement. After all, you may have other expenses—such as debt, emergency costs or child care—that seem more urgent.

Fortunately, you still have time left in the year to put money into your qualified retirement accounts. These accounts, like 401(k) plans and individual retirement accounts (IRAs), offer tax-deferred growth. That means you don’t pay taxes on growth inside the accounts until you take a distribution. Below are three commonly used qualified accounts and how they can help you save for retirement. You still have time left this year to ramp up your savings. Work with a financial professional to implement a savings strategy. |

Archives

November 2020

Categories

All

|

RSS Feed

RSS Feed

Thomas B. Scarpaci Jr., partnerJoseph D. Sciarrino, CPA, partner |

Site Map |

This information is designed to provide a general overview with regard to the subject matter covered and is not state specific. The authors, publisher and host are not providing legal, accounting or specific advice for your situation.

Securities and Advisory Services offered through CfreativeOne Securities, LLC Member FINRA/SIPC and an Investment Advisor. Financial Solutions Group, LLC and CreativeOne Securities, LLC are not affiliated.

This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

Check the background of an investment professional.

Securities and Advisory Services offered through CfreativeOne Securities, LLC Member FINRA/SIPC and an Investment Advisor. Financial Solutions Group, LLC and CreativeOne Securities, LLC are not affiliated.

This information has been provided by a Licensed Insurance Professional and does not necessarily represent the views of the presenting insurance professional. The statements and opinions expressed are those of the author and are subject to change at any time. All information is believed to be from reliable sources; however, presenting insurance professional makes no representation as to its completeness or accuracy. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

Check the background of an investment professional.